Business Owners

Strategies to help increase your personal cash flow, keep key employees and protect your business.

Financial Planning

Working closely with clients to achieve their financial goals.

Strategies for Families

Customized solutions based on you, plans for to accumulate and protect your wealth.

Incorporated Professionals

Tailored solutions to help you with your practice and personal cash flow.

Latest News

https://cathcartfinancial.ca/wp-content/uploads/2024/04/Optimizing-Wealth-Through-Asset-ReAllocation.jpg

300

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2024-04-03 13:40:022024-04-03 13:40:12Optimizing Wealth Through Asset Re-Allocation

https://cathcartfinancial.ca/wp-content/uploads/2024/04/Optimizing-Wealth-Through-Asset-ReAllocation.jpg

300

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2024-04-03 13:40:022024-04-03 13:40:12Optimizing Wealth Through Asset Re-Allocation https://cathcartfinancial.ca/wp-content/uploads/2024/01/Are-you-on-the-right-track-2.jpeg

750

1142

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2024-01-03 09:02:382024-01-03 09:02:49Are You On The Right Track?

https://cathcartfinancial.ca/wp-content/uploads/2024/01/Are-you-on-the-right-track-2.jpeg

750

1142

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2024-01-03 09:02:382024-01-03 09:02:49Are You On The Right Track? https://cathcartfinancial.ca/wp-content/uploads/2023/12/Prepare-in-Advance-for-Next-Years-Tax-Filing.jpg

833

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-12-01 06:02:212023-12-01 06:02:34Prepare in Advance for Next Year’s Tax Filing

https://cathcartfinancial.ca/wp-content/uploads/2023/12/Prepare-in-Advance-for-Next-Years-Tax-Filing.jpg

833

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-12-01 06:02:212023-12-01 06:02:34Prepare in Advance for Next Year’s Tax Filing https://cathcartfinancial.ca/wp-content/uploads/2023/11/Basic-Planning-for-Young-Families-reduced-copy.jpeg

667

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-11-01 07:02:322023-11-01 07:02:49Basic Planning for Young Families

https://cathcartfinancial.ca/wp-content/uploads/2023/11/Basic-Planning-for-Young-Families-reduced-copy.jpeg

667

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-11-01 07:02:322023-11-01 07:02:49Basic Planning for Young Families https://cathcartfinancial.ca/wp-content/uploads/2023/07/Can-probate-be-avoided-5.jpeg

340

475

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-07-03 09:44:172023-07-03 09:44:25Can Probate be Avoided?

https://cathcartfinancial.ca/wp-content/uploads/2023/07/Can-probate-be-avoided-5.jpeg

340

475

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-07-03 09:44:172023-07-03 09:44:25Can Probate be Avoided? https://cathcartfinancial.ca/wp-content/uploads/2023/04/Whole-Life-a-Whole-New-Investment-Class3.jpeg

199

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-04-01 08:02:012023-04-01 08:02:06Whole Life Insurance – A Whole New Asset Class

https://cathcartfinancial.ca/wp-content/uploads/2023/04/Whole-Life-a-Whole-New-Investment-Class3.jpeg

199

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-04-01 08:02:012023-04-01 08:02:06Whole Life Insurance – A Whole New Asset Class https://cathcartfinancial.ca/wp-content/uploads/2023/03/Estate-Equalization.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-03-09 13:16:182023-03-09 13:16:25Estate Equalization for Family Business Owners

https://cathcartfinancial.ca/wp-content/uploads/2023/03/Estate-Equalization.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-03-09 13:16:182023-03-09 13:16:25Estate Equalization for Family Business Owners https://cathcartfinancial.ca/wp-content/uploads/2023/02/ISTHEL_1.jpe

350

525

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-02-01 07:00:002023-02-01 07:02:05Is the Life Insurance Industry in Canada Stable?

https://cathcartfinancial.ca/wp-content/uploads/2023/02/ISTHEL_1.jpe

350

525

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-02-01 07:00:002023-02-01 07:02:05Is the Life Insurance Industry in Canada Stable? https://cathcartfinancial.ca/wp-content/uploads/2023/01/dont-wait-too-long-3.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-01-02 13:29:272023-01-02 13:34:56Don’t Wait Too Long to Convert Your Term Insurance

https://cathcartfinancial.ca/wp-content/uploads/2023/01/dont-wait-too-long-3.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2023-01-02 13:29:272023-01-02 13:34:56Don’t Wait Too Long to Convert Your Term Insurance https://cathcartfinancial.ca/wp-content/uploads/2022/11/Now-May-Be-a-Good-Time-to-Review-Your.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-11-01 06:30:002022-11-01 10:34:30Now May Be a Good Time to Review your Estate Plan

https://cathcartfinancial.ca/wp-content/uploads/2022/11/Now-May-Be-a-Good-Time-to-Review-Your.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-11-01 06:30:002022-11-01 10:34:30Now May Be a Good Time to Review your Estate Plan https://cathcartfinancial.ca/wp-content/uploads/2022/09/group-insurance-only-part-of-the-solution-3.jpeg

340

374

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-09-01 07:00:002022-09-01 07:36:35Group Life Insurance – Only Part of The Solution

https://cathcartfinancial.ca/wp-content/uploads/2022/09/group-insurance-only-part-of-the-solution-3.jpeg

340

374

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-09-01 07:00:002022-09-01 07:36:35Group Life Insurance – Only Part of The Solution https://cathcartfinancial.ca/wp-content/uploads/2022/08/is-i-time-for-your-insurance-audit-2-new.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-08-01 13:52:382022-08-01 14:00:21Is it Time for Your Insurance Audit?

https://cathcartfinancial.ca/wp-content/uploads/2022/08/is-i-time-for-your-insurance-audit-2-new.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-08-01 13:52:382022-08-01 14:00:21Is it Time for Your Insurance Audit? https://cathcartfinancial.ca/wp-content/uploads/2022/07/estate-planning-for-blended-families-4.jpg

340

533

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-07-06 13:09:572022-07-06 13:12:38Estate Planning for Blended Families

https://cathcartfinancial.ca/wp-content/uploads/2022/07/estate-planning-for-blended-families-4.jpg

340

533

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-07-06 13:09:572022-07-06 13:12:38Estate Planning for Blended Families https://cathcartfinancial.ca/wp-content/uploads/2022/03/Why-You-Should-Buy-Mortgage-Insurance-THUMBNAIL-AS2103.png

205

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-03-01 18:40:582022-03-01 18:41:10Why you should buy mortgage insurance through your life insurance advisor

https://cathcartfinancial.ca/wp-content/uploads/2022/03/Why-You-Should-Buy-Mortgage-Insurance-THUMBNAIL-AS2103.png

205

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-03-01 18:40:582022-03-01 18:41:10Why you should buy mortgage insurance through your life insurance advisor https://cathcartfinancial.ca/wp-content/uploads/2022/02/Having-Your-Cake-image.jpg

193

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-02-01 07:00:002022-02-01 07:06:05Having Your Cake and Eating it Too

https://cathcartfinancial.ca/wp-content/uploads/2022/02/Having-Your-Cake-image.jpg

193

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-02-01 07:00:002022-02-01 07:06:05Having Your Cake and Eating it Too https://cathcartfinancial.ca/wp-content/uploads/2022/01/Pay-attention-to-your-beneficiary-design.jpg

340

510

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-01-01 09:00:002022-01-01 09:06:05Pay Attention to your Beneficiary

https://cathcartfinancial.ca/wp-content/uploads/2022/01/Pay-attention-to-your-beneficiary-design.jpg

340

510

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2022-01-01 09:00:002022-01-01 09:06:05Pay Attention to your Beneficiary https://cathcartfinancial.ca/wp-content/uploads/2021/12/How-to-Protect-Your-Estate.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-12-01 06:00:002021-12-01 06:06:09How To Protect Your Estate

https://cathcartfinancial.ca/wp-content/uploads/2021/12/How-to-Protect-Your-Estate.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-12-01 06:00:002021-12-01 06:06:09How To Protect Your Estate https://cathcartfinancial.ca/wp-content/uploads/2021/08/Digital-assets.jpg

191

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-08-01 07:00:002021-08-01 07:09:12Have You Overlooked Assets in Your Estate Planning?

https://cathcartfinancial.ca/wp-content/uploads/2021/08/Digital-assets.jpg

191

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-08-01 07:00:002021-08-01 07:09:12Have You Overlooked Assets in Your Estate Planning? https://cathcartfinancial.ca/wp-content/uploads/2021/07/6-couple-in-kitchen-with-computer-and-coffee-smiling_BFVCU5RHj_thumb.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-07-01 07:00:002021-07-01 07:15:13Don’t Qualify For Traditional Life Insurance? Consider These Options

https://cathcartfinancial.ca/wp-content/uploads/2021/07/6-couple-in-kitchen-with-computer-and-coffee-smiling_BFVCU5RHj_thumb.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-07-01 07:00:002021-07-01 07:15:13Don’t Qualify For Traditional Life Insurance? Consider These Options https://cathcartfinancial.ca/wp-content/uploads/2021/06/All-in-the-Family-Estate-Plan-Farmers.jpg

201

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-06-01 06:00:002021-06-01 06:06:12All in the Family: Estate Planning for Farmers

https://cathcartfinancial.ca/wp-content/uploads/2021/06/All-in-the-Family-Estate-Plan-Farmers.jpg

201

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-06-01 06:00:002021-06-01 06:06:12All in the Family: Estate Planning for Farmers https://cathcartfinancial.ca/wp-content/uploads/2021/04/Who-Should-Own-My-Life-Insurance-image.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-04-01 06:00:002021-04-01 06:09:12Who Should Own My Life Insurance?

https://cathcartfinancial.ca/wp-content/uploads/2021/04/Who-Should-Own-My-Life-Insurance-image.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-04-01 06:00:002021-04-01 06:09:12Who Should Own My Life Insurance? https://cathcartfinancial.ca/wp-content/uploads/2021/02/small-business-3.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-02-01 16:49:562021-02-18 22:27:295 Top Financial Planning Strategies For Small Business Owners

https://cathcartfinancial.ca/wp-content/uploads/2021/02/small-business-3.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-02-01 16:49:562021-02-18 22:27:295 Top Financial Planning Strategies For Small Business Owners https://cathcartfinancial.ca/wp-content/uploads/2021/01/Impact-of-Recent-Events-on-Your-Estate-Plan.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-01-05 07:00:002021-01-05 07:09:10Impact of Recent Events On Your Estate Plan

https://cathcartfinancial.ca/wp-content/uploads/2021/01/Impact-of-Recent-Events-on-Your-Estate-Plan.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2021-01-05 07:00:002021-01-05 07:09:10Impact of Recent Events On Your Estate Plan https://cathcartfinancial.ca/wp-content/uploads/2020/12/Up-to-400-for-home-office-expenses.png

563

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-12-29 11:47:492020-12-29 12:24:20Government of Canada to allow up to $400 for home office expenses

https://cathcartfinancial.ca/wp-content/uploads/2020/12/Up-to-400-for-home-office-expenses.png

563

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-12-29 11:47:492020-12-29 12:24:20Government of Canada to allow up to $400 for home office expenses https://cathcartfinancial.ca/wp-content/uploads/2020/12/Highlights-of-the-2020-Federal-Fall-Economic-Statement@1000px.png

563

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-12-07 15:42:082020-12-07 16:15:49Highlights of the 2020 Federal Fall Economic Statement | Additional $20,000 CEBA loan available now

https://cathcartfinancial.ca/wp-content/uploads/2020/12/Highlights-of-the-2020-Federal-Fall-Economic-Statement@1000px.png

563

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-12-07 15:42:082020-12-07 16:15:49Highlights of the 2020 Federal Fall Economic Statement | Additional $20,000 CEBA loan available now https://cathcartfinancial.ca/wp-content/uploads/2020/12/How-Many-Wills-Do-I-need-main-image.jpg

199

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-12-01 07:00:002020-12-01 07:06:11How Many Wills Do I Need?

https://cathcartfinancial.ca/wp-content/uploads/2020/12/How-Many-Wills-Do-I-need-main-image.jpg

199

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-12-01 07:00:002020-12-01 07:06:11How Many Wills Do I Need? https://cathcartfinancial.ca/wp-content/uploads/2020/11/Diversiying-in-Uncertain-Times-article.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-11-01 07:00:002020-11-01 07:06:10Diversifying in Uncertain Times

https://cathcartfinancial.ca/wp-content/uploads/2020/11/Diversiying-in-Uncertain-Times-article.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-11-01 07:00:002020-11-01 07:06:10Diversifying in Uncertain Times https://cathcartfinancial.ca/wp-content/uploads/2020/10/preparing-your-heirs-for-wealth.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-10-01 07:00:002020-10-01 07:15:17Preparing Your Heirs for Wealth

https://cathcartfinancial.ca/wp-content/uploads/2020/10/preparing-your-heirs-for-wealth.jpg

200

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-10-01 07:00:002020-10-01 07:15:17Preparing Your Heirs for Wealth https://cathcartfinancial.ca/wp-content/uploads/2020/08/HOWWIL_1.jpg

166

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-08-04 12:32:382020-08-04 12:42:03How Will COVID-19 Impact the Insurance Industry?

https://cathcartfinancial.ca/wp-content/uploads/2020/08/HOWWIL_1.jpg

166

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-08-04 12:32:382020-08-04 12:42:03How Will COVID-19 Impact the Insurance Industry? https://cathcartfinancial.ca/wp-content/uploads/2020/07/CEWS_expanded@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-07-17 16:37:092020-07-17 17:09:18Canada Emergency Wage Subsidy expanded to include more businesses!

https://cathcartfinancial.ca/wp-content/uploads/2020/07/CEWS_expanded@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-07-17 16:37:092020-07-17 17:09:18Canada Emergency Wage Subsidy expanded to include more businesses! https://cathcartfinancial.ca/wp-content/uploads/2020/07/CEWS_extended_december@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-07-13 10:05:152020-07-13 10:36:23Canada Emergency Wage Subsidy extended into December!

https://cathcartfinancial.ca/wp-content/uploads/2020/07/CEWS_extended_december@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-07-13 10:05:152020-07-13 10:36:23Canada Emergency Wage Subsidy extended into December! https://cathcartfinancial.ca/wp-content/uploads/2020/07/Term-Life-Insurance-Two-Valuable-Options.jpg

208

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-07-02 17:27:552020-07-02 17:45:07Term Life Insurance – Two Valuable Options

https://cathcartfinancial.ca/wp-content/uploads/2020/07/Term-Life-Insurance-Two-Valuable-Options.jpg

208

300

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-07-02 17:27:552020-07-02 17:45:07Term Life Insurance – Two Valuable Options https://cathcartfinancial.ca/wp-content/uploads/2020/06/CERB_extended_CEBA_expanded@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-06-17 11:51:162020-06-17 12:30:16CERB Extended | Business Owners who did not qualify previously – expanded CEBA starts June 19th

https://cathcartfinancial.ca/wp-content/uploads/2020/06/CERB_extended_CEBA_expanded@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-06-17 11:51:162020-06-17 12:30:16CERB Extended | Business Owners who did not qualify previously – expanded CEBA starts June 19th https://cathcartfinancial.ca/wp-content/uploads/2020/06/insurancePlanningforBusinessOwnersFI.jpg

810

1440

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-06-01 17:27:242020-06-01 17:39:03Insurance Planning for Business Owners

https://cathcartfinancial.ca/wp-content/uploads/2020/06/insurancePlanningforBusinessOwnersFI.jpg

810

1440

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-06-01 17:27:242020-06-01 17:39:03Insurance Planning for Business Owners https://cathcartfinancial.ca/wp-content/uploads/2020/05/CECRA-May25.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-24 13:43:532020-05-24 14:15:14Small Businesses! Applications for Canada Emergency Commercial Rent Assistance starts May 25th

https://cathcartfinancial.ca/wp-content/uploads/2020/05/CECRA-May25.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-24 13:43:532020-05-24 14:15:14Small Businesses! Applications for Canada Emergency Commercial Rent Assistance starts May 25th https://cathcartfinancial.ca/wp-content/uploads/2020/05/CEBA_expanded.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-19 13:44:182020-05-19 14:12:13Expanded eligibility for CEBA $40,000 interest-free loan

https://cathcartfinancial.ca/wp-content/uploads/2020/05/CEBA_expanded.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-19 13:44:182020-05-19 14:12:13Expanded eligibility for CEBA $40,000 interest-free loan https://cathcartfinancial.ca/wp-content/uploads/2020/05/Canada-Pension-Plan.jpg

205

422

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-15 12:26:542020-05-15 12:36:08A Lifetime Gift for Your Grandchildren

https://cathcartfinancial.ca/wp-content/uploads/2020/05/Canada-Pension-Plan.jpg

205

422

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-15 12:26:542020-05-15 12:36:08A Lifetime Gift for Your Grandchildren https://cathcartfinancial.ca/wp-content/uploads/2020/05/CEWS_Extended@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-08 09:51:092020-05-08 10:39:17Extended! Canada Emergency Wage Subsidy extended beyond June

https://cathcartfinancial.ca/wp-content/uploads/2020/05/CEWS_Extended@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-08 09:51:092020-05-08 10:39:17Extended! Canada Emergency Wage Subsidy extended beyond June https://cathcartfinancial.ca/wp-content/uploads/2020/05/the-estate-bond-175x150-1.jpeg

150

175

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-01 11:40:402020-05-01 11:51:07The Estate Bond

https://cathcartfinancial.ca/wp-content/uploads/2020/05/the-estate-bond-175x150-1.jpeg

150

175

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-05-01 11:40:402020-05-01 11:51:07The Estate Bond https://cathcartfinancial.ca/wp-content/uploads/2020/04/CEWS_April27@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-21 13:52:372020-04-21 14:39:15Apply for Canada Emergency Wage Subsidy starting April 27th | Calculate your subsidy

https://cathcartfinancial.ca/wp-content/uploads/2020/04/CEWS_April27@2x.png

640

1000

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-21 13:52:372020-04-21 14:39:15Apply for Canada Emergency Wage Subsidy starting April 27th | Calculate your subsidy https://cathcartfinancial.ca/wp-content/uploads/2020/04/business-chairs-company-coworking-7070.jpg

423

640

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-16 13:23:282020-04-16 13:54:13New Canada Emergency Commercial Rent Assistance | Canada Emergency Business Account Expanded

https://cathcartfinancial.ca/wp-content/uploads/2020/04/business-chairs-company-coworking-7070.jpg

423

640

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-16 13:23:282020-04-16 13:54:13New Canada Emergency Commercial Rent Assistance | Canada Emergency Business Account Expanded https://cathcartfinancial.ca/wp-content/uploads/2020/04/CERB_expanded.png

320

500

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

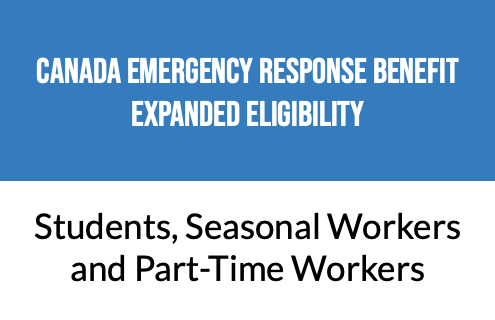

Cathcart Financial2020-04-15 09:49:412020-04-15 10:36:07Expanded eligibility for Canada Emergency Response Benefit (CERB) & Boosted wages for Essential Workers

https://cathcartfinancial.ca/wp-content/uploads/2020/04/CERB_expanded.png

320

500

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-15 09:49:412020-04-15 10:36:07Expanded eligibility for Canada Emergency Response Benefit (CERB) & Boosted wages for Essential Workers https://cathcartfinancial.ca/wp-content/uploads/2020/04/CEBA_Today.png

320

500

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-09 10:47:222020-04-09 11:12:12Applications for the Canada Emergency Business Account starts TODAY!

https://cathcartfinancial.ca/wp-content/uploads/2020/04/CEBA_Today.png

320

500

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-09 10:47:222020-04-09 11:12:12Applications for the Canada Emergency Business Account starts TODAY! https://cathcartfinancial.ca/wp-content/uploads/2020/04/Business_Owners_Qualification_850px.png

600

850

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

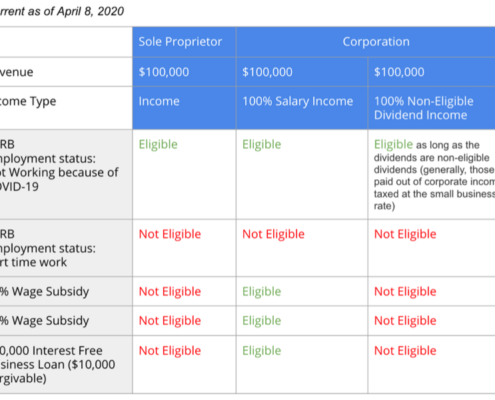

Cathcart Financial2020-04-08 15:50:562020-04-08 16:27:16Rules changed to allow more struggling business owners access to CERB, Wage Subsidy. Summer jobs program increased to 100%

https://cathcartfinancial.ca/wp-content/uploads/2020/04/Business_Owners_Qualification_850px.png

600

850

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-08 15:50:562020-04-08 16:27:16Rules changed to allow more struggling business owners access to CERB, Wage Subsidy. Summer jobs program increased to 100% https://cathcartfinancial.ca/wp-content/uploads/2020/04/GRANDF_1-175x150-1.jpg

150

175

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-02 10:06:222020-04-02 10:15:04Protecting Investments for Your Heirs

https://cathcartfinancial.ca/wp-content/uploads/2020/04/GRANDF_1-175x150-1.jpg

150

175

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-04-02 10:06:222020-04-02 10:15:04Protecting Investments for Your Heirs https://cathcartfinancial.ca/wp-content/uploads/2020/03/Trudeau-Wage_subsidy_75percent.png

337

500

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

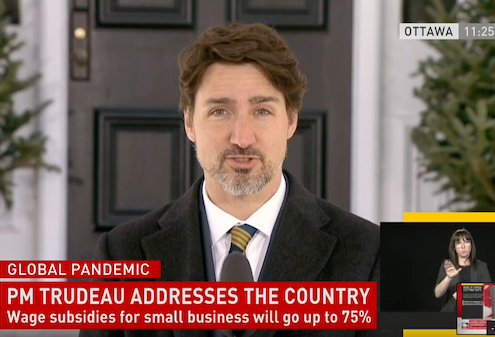

Cathcart Financial2020-03-27 11:40:562020-03-27 13:45:11Help for Small/Medium Businesses & Entrepreneurs – 75% wage subsidy, $40,000 interest-free loan & more

https://cathcartfinancial.ca/wp-content/uploads/2020/03/Trudeau-Wage_subsidy_75percent.png

337

500

Cathcart Financial

https://cathcartfinancial.ca/wp-content/uploads/2024/01/logo-space-1.png

Cathcart Financial2020-03-27 11:40:562020-03-27 13:45:11Help for Small/Medium Businesses & Entrepreneurs – 75% wage subsidy, $40,000 interest-free loan & more